Research by ALPHA

Author: Alpha

Calliditas is an orphan drug biotech developing Nefecon as treatment against kidney failure (IgA-nefrit). Nefecon, marketed as TARPEYO, gained accelerated approval in Dec'21 and full approval with extended label to protect the kidney function in December 2023. The company has a first-mover advantage and is at least 12-months ahead of the competition.

28/5 Japanese Asahi Kasei Corporation offered 208kr per share (a 80% premium). The share price was relative low at 113kr as a result from around 7% short positions. The offer is accepted by major shareholders and due diligence started. Let's see how the share price reacts when short positions must be covered in the coming months. My target includes a opportunistic premium.

Valuation (4)

First mover advantage

After the full approval in December'23 Calliditas ($600M) is one year ahead of its closest competitor Travere Therapeutics ($550M) with a similar market cap. The main driver for the company valuation in 2024 will be patient growth in the US and in other territories.

Both companies have significant short positions (increasing in Q4-23/Q1'24).

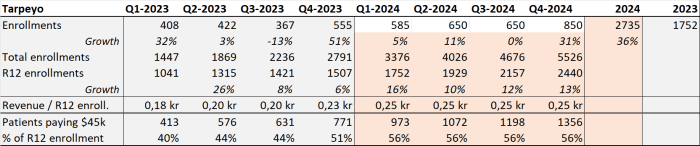

In Q4'23 Calliditas outperformed its closest competitor with 555 new patients (459). The company has a clear advantage in 2024 with Nefecon's full approval.

26/04/2024 by ALPHA|2Total addressable market

Calliditas estimates a $5-8B TAM for IgAN. In the US market the company operates with direct sales and in other regions it sells through partners receiving royalties between 10-30%.

06/04/2024 by ALPHA|2

06/04/2024 by ALPHA|2Profitability

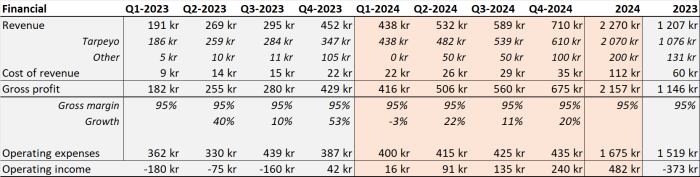

The path to profitability will drive the valuation in 2024. Operational costs are 400Mkr/quarter plus 50Mkr other expenses. The revenue per US patient is $15k per month. An average of 1000 active US patients per month should generate $45M (450Mkr) revenue per quarter for break-even results.

Key investment milestones:

- Q1 2024: cash-flow positive

- Q2 2024: profitable with >500Mkr revenue

- Q4 2024: >200Mkr profit (PE 7.5x on annual basis)

Assuming 80% growth in paying patients total revenue grows to 2.2Bkr in 2024 (1.2Bkr 2023).

06/04/2024 by ALPHA|2Short Positions

In April'24 short positions are above 7% (4M of 90M shares), which means 20 Days to Cover with an average daily volume of 200k. Analyst targets are 35% to 100% above current market price. The market is less optimistic about Calliditas sales growth.

Calliditas has a proven sales growth trajectory in 2022 and 2023. It's market position improved with the FDA full approval. I do not see a reason why the sales growth should not continue in 2024. There is room to grow in the addressable market.

In my opinion there is a lower downside risk and higher upside potential (incl. short-squeeze).

Comment below to share your thoughts.

06/04/2024 by ALPHA|2

Business (3)

Nefecon

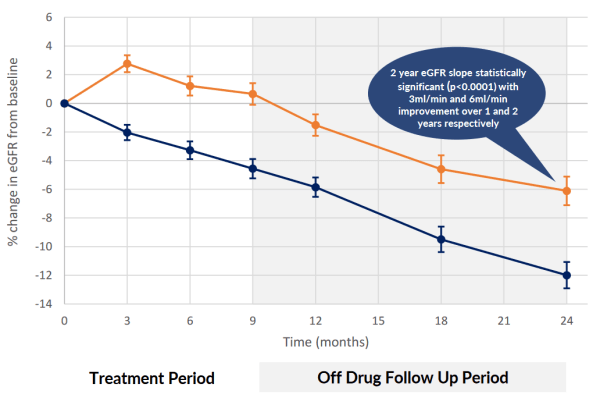

Nefecon is a disease modifying drug that improves estimated Glomerular Filtration Rate (eGFR), the primary indicator for the kidney function (filter). eGFR improved across the entire study population, independent of baseline UPCR (proteinuria) which positions the drug positive compared to competitors.

The working substance budesonide is a relative cheap corticosteroid or steroid (cortisone-like medicine). Nefecon is a patented and unique, oral medicine with targeted-release of budesonide. The medication significantly delays the need for kidney dialysis or transplantation.

FDA approval with extended label was based on Phase-3 study results that after 9-month of medication the improvement lasted until the end of the 24-months study for all patient groups.

In April'24 the company announced positive treatment response across the patient population!

26/04/2024 by ALPHA|1commercial approval

The company has full commercial approval for TAPEYO in the US. And the US patent is extended from 2029 to 2043.

In the EU/UK the drug is licensed to STADA and marketed as Kinpeygo. Approval applications are being reviewed and decisions are expected latest Q1-2024.

Everest Medicines is the Asia partner for Nefecon (approved in China in Dec'23).

Commission revenue from Asia could potentially reach 100Mkr in 2024 (based on Everest target).

VIATRIS is the selected partner for Japan.

05/04/2024 by ALPHA|2Setanaxib

Setanaxib is a potential drug for 4 different medications under development in Phase-2. Calliditas has not signed any partner agreements yet. Phase-2 study results are expected in 2024. This development is not calculated in the investment case.

05/04/2024 by ALPHA|1

People (1)

Renée Aguiar-Lucander

In the conference calls the CEO gives clear answers and demonstrates a good understanding of the business. She is able to explain medical terms and processes in common language.

2024 Tarpeyo targets are set with assumption of start-up friction for the new label.

26/04/2024 by ALPHA|1

Financial (3)

US sales

Nefecon (TARPEYO) is subscribed as a 9-months treatment at total cost of $135k per patient in the US. The product sells as 120x 4mg capsules for $15k that last 1 month. With direct sales in the US and through partners in other regions Calliditas has the potential for a strong sales growth in 2024-2026.

My expected TARPEYO enrollment and active patient growth results in higher sales (than company's guidance). With the assumption that the conversion ratio will improve after the commercial approval.

26/04/2024 by ALPHA|2FINANCIAL PROJECTION

In 2023 Calliditas under-performed on its own targets. Analyst expectations are that the 2024 target $150-180M for Tarpeyo sales is conservative. I estimate 2Bkr Tarpeyo revenue in 2024 and the company to be on track for 1Bkr net profit in 2025.

The company does not yet report any material sales in Asia, Europe/UK markets.

26/04/2024 by ALPHA|2Funding

After Q4'23 the cash position is 974Mkr. The company is sufficiently funded and share dilution is unlikely.

26/04/2024 by ALPHA|2

Risks (3)

Roll-out

The paying subscription has been slower then expected in 2023 as patients are awaiting approval for the prescription from commercial insurers. It takes more time than analysts expected to increase sales.

The company announced in the 2023 annual meeting that some friction can be expected with establishing the new label after full approval in the US. An important risk to monitor for investors in the first half of 2024.

06/04/2024 by ALPHA|2Competitors

Travere Therapeutics offers the only Tarpeyo alternative for US patients with the conditional approved FILSPARI. FILSPARI requires 24 months treatment (vs Trapeyo 9M). FILSPARI received accelerated approval with a Risk Evaluation and Mitigation Strategy (REMS) requirement. The application for full commercial approval was delayed in 2023.

After the December'23 meeting with the FDA the competitor announced additional focus on approval for FILSPARI with a supplemental New Drug Application (sNDA) in Q1-24. For FSGS the FDA communicated that Phase-3 results alone are not sufficient to support an sNDA submission.

Calliditas is at least one year ahead (based on 10 months approval timelines).

Swiss Novartis is a another competitor that has produced first Phase-3 results and plans to apply for FDA Accelerated approval in 2024. The company is at least two years behind Calliditas. Novartis has the resources to start a sales campaign after Accelerated Approval.

Other competitors are; Vera Therapeutics,.....?

06/04/2024 by ALPHA|2Reduced treatment period

There is a risk that the treatment period is reduced from 9-months to 3-months. As shown in the below chart there is no meaningful effect, compared to the baseline, after the first 3-months. On the positive side this change could increase repeat treatments. Most likely at a lower annual cost per patient.

05/04/2024 by ALPHA|2

05/04/2024 by ALPHA|2