Research by ALPHA

Author: Alpha

- 12.00 +78.31% (03/11/2026)

- BUY

Stillfront is a Swedish gaming company focused on mobile- and web-gaming. In the past 5 years the company lost 95% of its market cap with a share price decline from above 100kr to below 5kr. However in recent months the share recovered 40% as management makes progress.

This is a possible turn-around case after 250Mkr cost reduction,reduced debt and focus on profitability across the portfolio, currently valued just above 0.5 P/B. The Q3 2025 report showed first results with 0,11kr EPS. A short-term investment with >50% potential upside from 6.5kr.

Valuation (3)

EBITDAC multiple

At the time of writing Stillfront is valued at ≈3.5Bkr (price 3.75kr) which is less than 5x EV/EBITDAC (1.623Mkr/TTM) with 4.381Mkr net debt.

In November 2024 Embracer sold Easybrain at a valuation of 9.3x EBITDAC.

Easybrain specializes in a narrow, high-volume casual puzzle niche, while Stillfront is a diversified holding company with a broad portfolio of games across multiple genres and platforms. The two companies cannot be directly compared, but Stillfront looks cheap at current valuation.

Assuming a valuation in the mid-range between these two valuations, 7x EV/EBITDAC, adds almost 80% upside above 12kr. This calculation is based on current profitability, with management focus on its current games portfolio and improving the balance-sheet, without acquisitions.

14/11/2025 by ALPHA|1Share repurchase

On 23rd October the board decided to active the mandate for the re-purchase of 210Mkr shares (before the next annual meeting), which is about 6% of its market-cap. The shares will be used for earn-out payments and therefor return to the market (after lock-up). This reduces possible shares dilution from earn-outs at the expense of cash.

13/11/2025 by ALPHA|1Analyst price targets

Analyst see potential upside between 50-100% from 6.5kr.

Analyst

updated

Price

Cantor

21-Oct-2025

14,00

Kepler

28-Oct-2025

12,00

Pareto

24-Oct-2025

9,00

03/11/2025 by ALPHA|1

Business (3)

Direct-to-Consumer (DTC) Developments

Stillfront has significantly expanded its direct-to-consumer (DTC) share, increasing from 26% in 2023 to 39% in Q2 2025, and 44% in Q3 2025. This shift has contributed to improved gross profit margins, as DTC channels offer higher margins compared to third-party platforms.

14/11/2025 by ALPHA|1Key franchise reviews

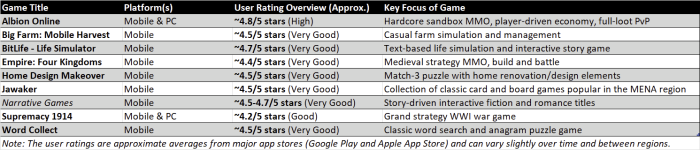

In general Stillfront's Key Franchise games receive good reviews and the company focuses its product development on games to improve profitability (over UA and pure revenue).

14/11/2025 by ALPHA|1

14/11/2025 by ALPHA|1Mobile Gaming Sector Growth

Stillfront's free-to-play and mid-core games can leverage on AI-driven personalization and expanding in high-growth regions (e.g., Asia-Pacific).

- Analyst expect ~10% CAGR in the mobile gaming sector through 2029.

- AI, 5G, and multiplayer trends are shaping the industry.

- Advertising and in-app purchases remain key revenue drivers.

- Infrastructure and regulatory challenges could pose risks in emerging markets.

11/11/2025 by ALPHA|1

People (2)

CEO Alexis Bonte

Alexis Bonte serves as Stillfront CEO since March 2025, having previously held the role of Interim CEO. He restructured the company in three geographical areas with a flatter organization and focus on profitability (presented in the earnings call Q4 2024). This also resulted in a large asset write-off on North America.

Alexis Bonte owns >1.2M shares.

14/11/2025 by ALPHA|1Insider transactions

Board member Marcus Jacobs increased his position with several transactions in 2025. Beginning november 2025 he increased his position with 65%.

11/11/2025 by ALPHA|1

Financial (2)

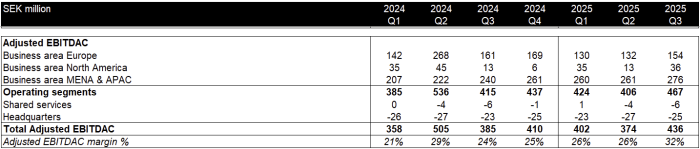

EBITDAC RESULTS

EBITDAC is a performance metric defined as profit before interest, tax, depreciation, and amortization, less capitalized product development.

The metric provides a clearer view of the underlying cash-generating performance, as capitalized product development represents a regular and necessary use of cash within operations (regular personal expenses).

The EBITDAC improved with falling revenues, which indicates the company successfully allocated UAC spending and product investments to prioritize profits over revenue growth. The MENA & APAC business is most successful, North America indicates a turn-around, and profits in Europe are declining. These shifts resulted overall in better margins.

13/11/2025 by ALPHA|1Financial strength

Stillfront has a higher financial risk profile compared to its peers based on financial strength ratios.

Ratio

Value

Comments

Equity ratio

50%

Lower equity to asset ration than peers (80%)

Net debt

30%

Higher net debt to total assets ratio

Debt to equity

1.1

Higher debt to equity ratio than peers (0.2-0.7)

NET DEBT/EBITDA

2.1

Decreased and closer to target of 2

In the past year the company significantly reduced its total liabilities to 7.2Bkr (8.3Bkr). The net debt/EBITDA ratio is almost at the target value of 2, based on debt including earn-out obligations. The company has a cash position of 773Mkr at the end of Q3 2025.

Debt maturity 2.9Bkr in 2027 (excluding earn-outs).

Based on the debt maturity with earn-outs in 2026, and first bond maturity in July-2027, the company uses FCF for share re-purchase (at 0.5x book-value), and is expected to restructure debt in 2026 prior to the maturity. The strategic review could also lead to the sale of assets that are not Key Franchises to de-risk the balance-sheet and focus on the profitable business.

13/11/2025 by ALPHA|1

Risks (1)

Continued revenue decline

A continued decline in revenue caused by reduced UA and fierce competition in the mobile gaming market. E.g. management indicated that in Q1 2025 UAC increased caused by more competitive bidding.

13/11/2025 by ALPHA|1