Research by ALPHA

Author: Alpha

- 21.80 +32.85% (06/11/2025)

- 20.00 +21.88% (20/02/2025)

- HOLD (BUY)

SBM Offshore is an investment in long-term contracts and cash-flow in the oil industry. The offshore company builds and operates FPSO (Floating Production Storage and Offloading) platforms (that produce around 2 million barrels per day).

After a positive Q2'24 the company increased 2024 targets and doubled its share repurchase program.

The investment case is based on the Lease and Operate business with double digit growth and 50% EBITDA margin. This segment provides a sound basis for annual cash flow. The company is undervalued at 6x 2023 EPS. Priced at €16 the company returns a 10% cash yield with >20% margin of safety on its 2025 earnings potential.

Valuation (3)

Sideways share price

On a five year chart the stock price has mainly moved side-ways. SBM Offshore has not been able to translate growing back-log with long-term contracts and valuable assets into a higher share price. Investor interest in the company has been low, which could be explained by; ESG policies by institutional investors, the complexity of the accounting and volatility of earnings from turnkey projects.

SBM has however improved its ESG profile and improved quality of earnings. I expect the valuation to improve in the next 12 months.

After the Q2'24 rally the share price is back to its 2020 level. EPS increased 150% between 2020 and 2023 under IFRS accounting. The quality of the revenue/profits from Lease and Operate ($2-2.5 EPS) are not reflected in the share price.

Furthermore the Fast4ward approach with reserved hulls also makes the Turnkey segment more attractive to deliver better profits, reduce risk, improve cash-flow and balance sheet.

EV/EBITDA is close to 5 year average 8x (with Directional net debt €7.1B).

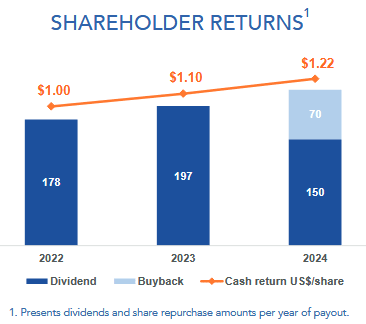

16/10/2024 by ALPHA|1Shareholder returns

The company policy is to provide a stable annual return with the flexibility in form of dividend and/or repurchase of shares from €3B market cap.

Share buyback increased with €65 million by the end of April 2025.

09/08/2024 by ALPHA|1Backlog

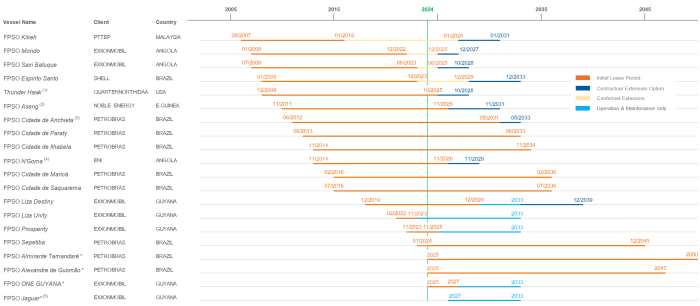

The company has a contractual backlog that gives good visibility into future cash-flows. The segment Lease- and operate shows steady growing cash-flows based on long term contracts.

09/08/2024 by ALPHA|1

09/08/2024 by ALPHA|1

Business (5)

Lease and Operate

This segment contains 17 FPSO's with long term contract to Tier-1 oil companies. In 2025 the company will add 3 additional FPSO's in production. 2 platforms will be sold to become Operate and Maintenance.

The total of 20 platforms is an interesting portfolio of Assets under Management to optimize with new lease contracts, platform sales to operate only and new constructed platforms to add. The 2024 result show that the business is just as profitable with somewhat lower oil prices ($70-80 per barrel).

10/08/2024 by ALPHA|1Turnkey FPSO projects

SBM Offshore has 3 FPSO(s) under construction for delivery in 2025 with > 75% completion. Project results and asset development will materialize in the next 12 months.

The company regularly creates standardized hulls that are sold to shorten delivery times for the platforms. This is an attractive business model for the company and for its customers.

10/08/2024 by ALPHA|1Floating Production Storage and Offloading

SBM Offshore activities are the design, supply, installation, operation and life extension of Floating Production Storage and Offloading (FPSO) vessels. These are either leased to clients or supplied on a turnkey sale basis. FPSOs process well fluids into stabilized crude oil for temporary storage on board, before being transferred to a shuttle tanker for export from the field. Oil and gas enhanced recovery systems − such as water injection, gas injection, chemical injection and gas lift systems − are used to improve efficiency and production levels.

The FPSO proposition is competitive with its Fast4ward approach and lower emissions than industry average. Latest FPSO designs include CO2 removal from gas streams for re-injection into the well offshore.

FPSO's are competitive oil platforms with break-even at $20-35/boe (barrel oil equivalent).

10/08/2024 by ALPHA|1Renewable energy

SBM Offshore has offshore products for renewable energy e.g; Floating Offshore Wind (FOW), Wave Energy Capture (WEC) - piloted in France - and offloading Carbon Dioxide. It provides anchoring technology for the offshore energy market.

The renewable energy is not a significant part of the business (yet), but more a field for innovation.

09/08/2024 by ALPHA|1Net zero strategy

SBM Offshore's strategy is to be aligned with the transition to net zero by 2050. Focusing on deep-water oil production taking part in the energy transition producing fossil fuels at lower CO2 emission. SBM is investing to keep a leading role.

MSCI upgraded the ESG rating of SBM Offshore from A to AA, recognizing SBM Offshore’s environmental management systems and its industry leadership in managing carbon emissions.

09/08/2024 by ALPHA|1

Financial (2)

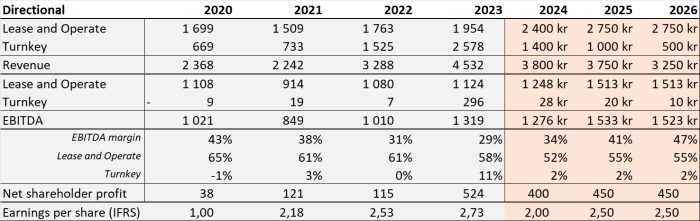

Directional earnings

In the coming years the companies more profitable Lease and Operate (50-60% EBITDA margin) business is expected to continue to grow. This should improve the quality of the directional earnings as reducing the weight of Turnkey.

The $1.2B EBITDA guidance leaves room for $700-800M ($600M in 2023) interest payments and $400-500M profit before tax.

09/08/2024 by ALPHA|1Debt

The debt is split into $4B non-recourse (asset backed) financing in SPVs and $5B borrowing for the ongoing construction of FPSO(s). The ongoing projects will become non-recourse when going into production.

The debt levels do not seem to worry credit providers supplying $3.2B credit in 2023.

09/08/2024 by ALPHA|1

Risks (1)

Financial market ESG policy

The ESG policies constrain exposure by financial institutions towards fossil fuel financing. This is a risk for SBM to finance ongoing projects and sign new deals. Interest rates are higher than before and the ESG policies further increase financing costs.

09/08/2024 by ALPHA|1