Research by ALPHA

Author: Alpha

- 28.90 +8.65% (06/11/2025)

- 30.00 +12.78% (08/09/2025)

- SHORT-LIST (SELL)

Railcare provides railroad (transport) services in Sweden. Its market is expected to grow supported by several long-term trends. Railcare has set financial goals for 2027 to grow revenue and improve its operating margin.

The share price developed strong in the first three quarters of 2024 based on the company results and analyst coverage that triggered growth in private investors. In the past 6 months the share price corrected due to lower margins and EPS. Expected growth in revenue has not yet materialized.

In Q1 2025 revenue and operating margin declined with a significant impact on EPS. The company needs strong reports in the coming quarters to justify its PE ratio >20x. In the long term Railcare is a defensive investment supported by positive market trends. On my short-list for for better buying opportunities (<25kr) as profitability is lagging.

Valuation (1)

High PE VS fair value

Railcare is currently priced at 22x earnings per share after Q1 2025. Management states a negative impact on margins to prepare the organization for growth, and continued disappointing results in the UK.

The revenue growth from new contracts and recovery of EPS are priced in at 26-27kr. The market is forward looking towards better results in 2025 and expected EPS growth in the coming years. The share price is based on expectations that financial goals are achieved, but is >30% overvalued related ot current performance of rolling 12 months.

15/10/2025 by ALPHA|1

Business (3)

Electric locomotive

Railcare developed an electrical locomotive with battery systems. This Multi Purpose Vehicle is firstly developed for Railcare's own use. The company has a limited technology sales track record.

German studies indicate that hybrid and battery locomotives are significant cheaper, up to 80%, than hydrogen driven. My expectation is that hydrogen is the preferred technology in heavy transport given the high energy density (lower weight).

Locomotives in general are old and dirty machines with high maintenance costs that sooner or later must be replaced with environmental friendly alternatives. This could trigger a change in the sales of electrical locomotives. External sales of MPV's would be a true catalyst, but with a low probability.

18/09/2025 by ALPHA|3Market trends

Railcare benefits from several long-term trends, including environmental friendly transport, establishment of new business in northern Sweden and Sweden's NATO membership with increased defense readiness.

Since Apil'23 EU C02 emission rights policy includes transport, which benefits rail transport.

18/09/2025 by ALPHA|2Business segments

Railcare provides railroad services; Enterprise (35%) includes railroad maintenance and projects, Transport (50%) and Technology (15%). A good services mix; the Transport segment is more cyclical, while the Enterprise segment depends mainly on government budgets.

The market mix makes the company less sensitive for the economic cycle. This fits the cost structure with relative high fixed costs for its assets and lease-rental agreements. Long-term agreements are needed on both sides of the book.

UK/International enterprise business is not profitable and requires a change of strategy.

18/09/2025 by ALPHA|1

People (2)

Major shareholder

Major shareholder Treac sold its 10% holdings to Swedia Capital controlled by Staffan Persson. The transaction is a positive indication for further growth.

09/07/2025 by ALPHA|1Management

The company is strengthening its management to prepare the organization for further growth.

21/03/2025 by ALPHA|1

Financial (2)

Financial goals

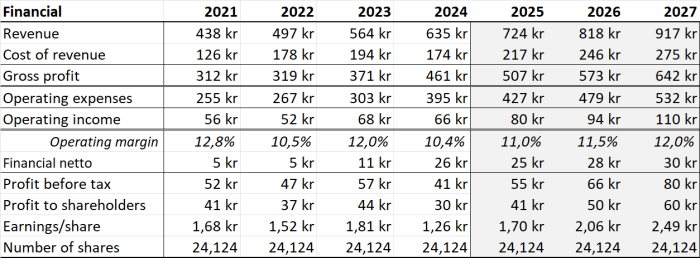

In beginning of 2024 the Railcare board announced new financial goals for 2027 to reach 1.000Mkr revenue with 13% operating margin. This indicates that earnings per share can increase from 1.80kr to 3.00kr.

It must be noted that the margin improvements is also a result of the changed IFRS 16 interpretation that moves leasing cost from operational expenses to financial!

Past results do not support that these targets will be achieved. It would require a positive improvement from the trend in CAGR and the operational margin.

09/07/2025 by ALPHA|2Financial results

In the coming years Railcare expects to grow its business in Transport, Enterprise and technical services (Lokverkstaden). The below model is more conservative than the financial goals by Railcare. It estimates earnings to increase to 2.50kr per share with growing revenue and improved profitability. The past revenue growth does not support >15% CAGR to reach the financial goal of 1Bkr revenue. Also the required investments in growth put pressure on the operating margin.

Overall Railcare delivers stable growth in its markets, but earnings per share are volatile and lagging. When the company improves operating margins again the earnings per share can grow to around 2.50kr.

Notes:

- Leasing contracts are partially in EUR, the stronger SEK will reduce leasing costs in 2025.

- Profitability should improve with activation of new contracts in 2025.

- Reporting is adjusted for leasing obligations to IFRS16, which impacted assets and liabilities on the balance sheet, increased profit margins and the financial costs since the 2024 report.

09/07/2025 by ALPHA|1

Risks (2)

Low liquidity

Liquidity is very low and sometimes below 10k/day. On the other hand this can also offer swing trading opportunities.

18/09/2025 by ALPHA|1UK business

The losses in the UK business are a risk for the growth plans. It draws (financial) resources that are better used elsewhere to realize the growth strategy. This is an Achilles' heel for years that the company does not act upon. There seems to be potential for international growth, but the company is not able to realize this.

21/03/2025 by ALPHA|1