Research by ALPHA

Author: Alpha

Centrus investment case is a bet on the revival of nuclear energy as part of the global energy transition. The case is supported by recent announcements for nuclear power supply to data-centers.

This US based supplier of LEU (>$200M) and enrichment technical services (>$100M), with customers in the US, Asia and Europe, operates the only facility licensed by the U.S. Nuclear Regulatory Commission (NRC) to produce HALEU (20% U-235). HALUE is the fuel required for many types of Small Modular Reactors (SMRs). Centrus is at least 5 years ahead of competition on High-Assay Low Enriched Uranium.

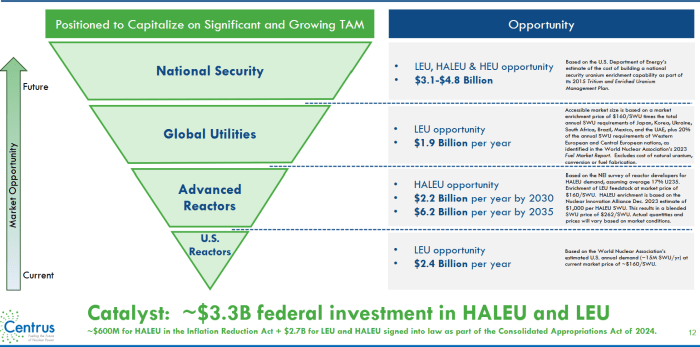

Future demand for HALUE and the sanctions on Russian LEU (30% of US/EU demand) are multi-billion dollar growth opportunities for Centrus in the coming 10 years. The US government stimulates investments with RFPs for LEU (3.4B$) and HALUE (2.7B$).

In the short term the supply by TENEX is a risk for revenue and profits. In the long term (3-5 years) Centrus can become a global player in nuclear enrichment. A long term hold in the portfolio to invest in the energy transition.

Valuation (5)

Sentiment 2024

Market sentiment started to change mid-September'24 when Centrus was valued less than 10x my estimated earnings for 2024. Within a month the price increased with 100%.

In October news from Microsoft, Google and Amazon to invest in nuclear energy supply in various ways confirmed the thesis that nuclear power is needed for data-centers.

The DOE awarded Centrus in two HALUE RFPs (de-conversion and enrichment), and the LEU enrichment RFP. The size of these awards are not published, but can reasonably be expected to >$1B.

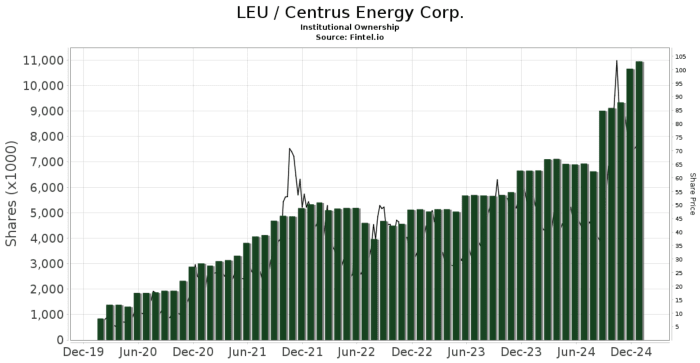

Institutional investors increased holdings in 2024. In December 2024, after the sanction by Russia and the convertible note when the priced declined 30%, institutional holdings continued to increase to about 70% of shares outstanding.

Centrus, as nuclear fuel supplier, has a lower risk profile compared to the listed SMR development companies that compete against major industrial competitors (e.g. GE Hitachi, Westinghouse, Rolls Royce). SMR companies develop reactors, which are high risk projects that require large investments and regulatory approval. Whereas Centrus has a proven and operational centrifuge enrichment technology (approved by the NRC).

04/02/2025 by ALPHA|1Regulated market

Centrus operates in a highly regulated market as nuclear fuel broker (LEU) and technology provider (LEU/HALUE). The company developed the AC100M centrifuge for HALUE production on American Centrifuge technology. The complex and highly regulated centrifuge technology are the companies moat. The required investment in technology, a safe facility and the regulatory process are hurdles for potential competitors (est $300-$500M minimal initial CAPEX).

It is the only company licensed to produce HALUE in this heavily regulated market. The only commercial enrichment facility for LEU in the US is operated by Urenco.

The market is also regulated by proliferation agreements which restricts foreign competition.

04/02/2025 by ALPHA|2History

In 2014 Centrus Energy emerged from Chapter 11 restructuring of former USEC (United States Enrichment Corporation). USEC was founded by privatization of US nuclear enrichment activities in 1995 through the USEC privatization act. USEC failed previously as its investment to establish nuclear enrichment capacity in the US did not get the required government support.

After the earthquake and tsunami in Japan 2011 there was an over-supply of nuclear fuel. In addition this was followed by reactors being closed down (especially in Germany and Japan). And subsidized competition from renewable energy threatened profitability. The market reached a bottom in 2018 and started to recover. Since 2022 nuclear energy is seen as viable solution to reduce CO2 emission. The market is now expected to grow in the coming decades.

03/02/2025 by ALPHA|2Global 'green' demand

There are three trends supporting the growing need for green electricity in the future:

- Replacement of fossil-fuels as source for 60% of electricity production.

- Electrification as part of the green transition towards carbon-free energy.

- Increasing electricity demand by; data-centers, AI and a growing population.

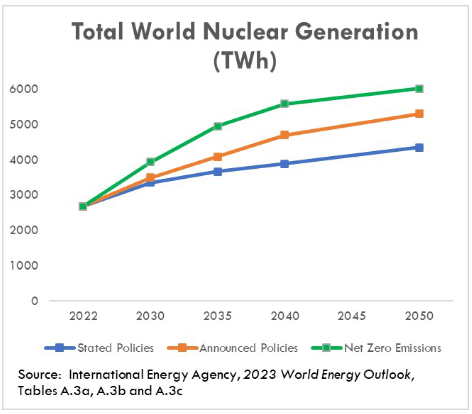

The demand for nuclear energy can be expected to triple in the next 10-20 years as part of the green transition. In optimistic scenario's the growth can even be a factor 10-20x current supply. Globally new government initiatives and funds are made available to develop nuclear power facilities.

UK government announced £300M investment in HALUE (2024-01-07).

Wind and solar as sources will not be able to meet electricity demand instantaneously and reliable over time. Nuclear energy is required for base-load and to respond to demand-supply in-balance.

03/02/2025 by ALPHA|2Data-centers

The energy demand for data-centers, especially for AI, is increasingly becoming a topic. This electricity demand requires base-load power. Intermittent cannot supply the continuous power demand.

Microsoft deal to purchase the electricity from Three Mile Island Unit 1.

The investments in data-centers for AI and cloud services are drivers for investments in nuclear energy that drive valuation higher based on the new growth opportunities.

26/09/2024 by ALPHA|1

Business (4)

HALEU demand

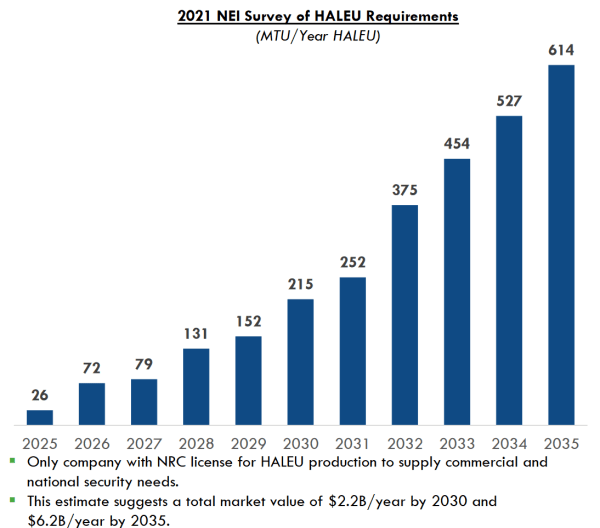

HALUE will be needed to support the 9 committed/ongoing SMR design projects in the US. The DOE drafted an RFP for the purchase of 145 MTU in 10 years. The HALUE market is expected to growth from $100M in 2025 to over $2B by 2030.

SMR's are factory produced nuclear power facilities. The CO2 foot-print is similar to other green energy sources (11-12gCO2e/kWh vs Hydro 24g, Solar 40-50g). Market expectations are that SMR's will come into production after 2030.

Investments in SMR nuclear technology are e.g:

- DOD selected BWXT for Project Pele to develop a prototype (container sized) portable SMR to be delivered in 2025. The reactor is using HALUE TRISO fuel.

- US Air Force selected OKLO to site, design, construct, own and operate a microreactor facility for its airbase in Alaska. OKLO has a MOU with Centrus.

- Terrapower started the construction of its Natrium reactor in Wyoming.

03/02/2025 by ALPHA|2Technical solutions

This segment includes technical service, development of centrifuge technology and the HALUE services contract. The government support will trigger investments in enrichment capacity and an increased demand for centrifuge technology.

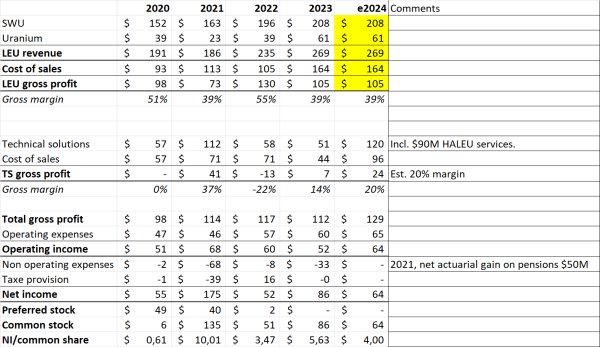

The Phase-2 HALUE contract is a full year of operations to deliver 900Kg of HALUE (2024) with a value of $90M. The contract has been extended and expanded to resolve issues with the 5B Cylinders to hold the fuel. After the initial 900kg the contract has the potential to be extended for 9 years at approximately $100M per year.

Other contracts:

- X-Energy to support the design of the "TRISO"-fuel manufacturing process (2021-2027).

03/02/2025 by ALPHA|2LEU

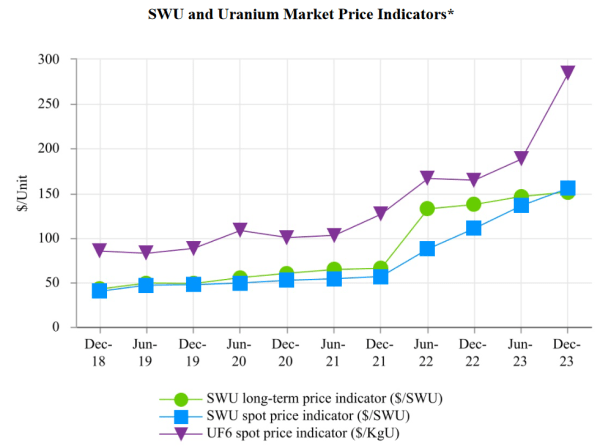

The LEU segment currently represent the larger part of Centrus revenue (80%). Since 2018 the LEU market has recovered including price levels. With the dominant Russian market position (40%) and the current geo-political situation it can be expected that prices remain high.

On the other hand the sanctions by the Russian government (November 2024) could cut Centrus supply from TENEX, and is expected to have an impact on profitability.

The TENEX contract has a low SWU price until 2028 after the 2018 price reset.

03/02/2025 by ALPHA|2Strategy

Centrus was mainly a broker in the supply chain, selling Russian LEU in the US, and started to change its strategy in response to new opportunities (to establish US enrichment capacity). The strategy is aimed at both the commercial market and the government market, that requires compliance with US National Security policy.

The success of the strategy will (also this time) be determined by winning government support. The CAPEX will be a shared private and government investment, that could result in share dilution. Centrus estimates 42 months lead time for new enrichment capacity, which means no earlier than Q1 2028.

$350M senior convertible note at 2.25% as private investment in November 2024.

With its strategy Centrus aims to become a major player in the large nuclear fuel market.

03/02/2025 by ALPHA|2

03/02/2025 by ALPHA|2

People (1)

CEO Amir Vexler

The CEO Amir Vexler has a long background in the industry. The company won DOE RFP awards, $2B LEU contracts, and executed a private placement of $350M under his leadership.

The CEO has only a limited equity position in the company.

03/02/2025 by ALPHA|1

Financial (4)

Historic financial position

Centrus is the successor to USEC that emerged from bankruptcy protection in 2014. Due to this history the company had issued preferred shares, uncovered pension obligations and a negative equity value.

Most of the issues on the balance sheet are resolved in 2023. In 2024 almost all pension obligations are sold to insurance companies, often with a net profit.

Net income will be less volatile without major non-operational income/expenses.

04/02/2025 by ALPHA|2COMMON stock

In 2021 Centrus repurchased all of its preferred stocks in exchange for common stock and a warrant to purchase 250.000 shares at $21 for a non-cash exchange against $5M liquidation preferences. The warrant expired in Feb'24. A transaction with >10% shareholder Morris Bawabeh (Kulayba LLC).

The common stock position improved with all preferred stock related issues resolved! Earning are as of 2023 fully attributed to common stock.

07/08/2024 by ALPHA|2Earnings

With the current market conditions the LEU results can be expected to be unchanged in 2024. The technical solutions segment will be stronger with the $90M HALUE contract. With these assumptions I expect at least $4/share.

07/08/2024 by ALPHA|1

07/08/2024 by ALPHA|1Deferred revenue and margins

Deferred revenue liability is 35% of the balance sheet. This can impact revenue to cash conversion and the gross profit margin. From the reporting it is not totally clear how the company is contractual exposed or hedged. Although, in the 2023 shareholder letter the CEO announced an improvement in margins.

07/08/2024 by ALPHA|2

Risks (5)

Tenex supply contract

In October 2020 the US extended the 1992 Russian Suspension Agreement for nuclear fuel to be exported to the US. The Russian company TENEX is a major supplier of SWU to Centrus. Centrus typically supplies the uranium to TENEX in return for LEU after SWU. The company must purchase a minimal amount of SWU until 2028. The purchase obligation exceeds the Centrus order book and requires new sales.

The TENEX contract is a risk for the supply with the current geopolitical situation. The supply contract is the source for 50% of customer delivery through 2027. This is difficult to replace in case of sanctions.

Centrus has a similar supply contract until 2030 with French Orano that could also supply SWU.

In May'23 the US imposed restrictions for Russian uranium/LEU import. Currently Russia has 40% of the global uranium enrichment capacity, and the rest of the world does not have sufficient enrichment capacity to fuel nuclear power stations. Replacement of the Russian capacity is a potential catalyst for Centrus. The geopolitical situation could also become a business driver!

In November the Russian government sanctioned export of enriched uranium.

04/02/2025 by ALPHA|2Continuous dilution

In the past 10 years there has been a continued share dilution. Partially to resolve balance sheet issues, but also by printing new shares for management.

03/02/2025 by ALPHA|1Nuclear accident

A nuclear accident could revert the positive change in public opinion from the recent years. Such an event could have a negative impact on the valuation.

06/10/2024 by ALPHA|1Legal exposure

Several court cases are ongoing in the US related to past operations (at the Portsmouth GDP in

Piketon, Ohio).07/08/2024 by ALPHA|2ASSET OWNERSHIP

Centrus has a lease agreement with the DOE for the Piketon facility and an operations agreement for HALEU production. The title to the facility and equipment are stated in the reporting:

Any facilities or equipment constructed or installed under the HALEU Contract, or other contract with DOE will be owned by DOE and may be returned to DOE in an “as is” condition at the end of the lease term. DOE will be responsible for the D&D of any returned facilities or equipment. If we determine the equipment and facilities may benefit Centrus after completion of the HALEU program, we can extend the facility lease and ownership of the equipment will be transferred to us, subject to mutual agreement regarding D&D and other issues, including those impacted by DOE’s recent decision to competitively award a separate contract for operations of the HALEU cascade following the expiration of our HALEU Contract, which may be awarded to a third party.

The lease agreement and ownership is a potential risk for the value of the company.

07/08/2024 by ALPHA|2