Research by ALPHA

Author: Alpha

- 19.82 +2.67% (07/11/2025)

- 16.00 -17.10% (03/11/2026)

- SELL (HOLD)

Fortum is a defensive utilities investment in a quality company with a strong balance sheet. The company strategy is to focus on core business, and divesting non-core assets.

In the energy market Fortum is well positioned providing base-load and flexible energy capacity in the Scandinavian market. 90% of EBITDA results from 45TWh low CO2 hydro and nuclear power generation at competitive prices.

After the recent run in Q3 2025 Fortum is valued at >20x TTM earnings, which looks over-valued given expected future earnings. I think it is time to take some profits and changed to Sell (Hold).

Valuation (3)

Prudent strategy

After the Russian invasion into Ukraine in 2022, Fortum was forced to sell Uniper to the German state caused by giant losses on gas contracts in Germany. A year later the company also lost control over its Russian assets that are no longer reported upon!

From 2023 Fortum focused on its core-business with clean-energy in the Nordics. Its strategy being more prudent in risk management and cash management. Being more prepared for market volatility and geopolitical developments. With 51% ownership by the Finish state the priority is to focus on reliable, clean and cheap energy production.

The company now has a strong balance sheet, cash and cash-flow, better cost control and focus on its core business. Fortum has an excellent position for growth investments and/or to increase direct shareholder cash returns.It makes (smaller) investments in renewable energy, nuclear energy (lifetime extensions), and preparing sites for industry and data-centers.

Management is prudent given the risk from high volatility in energy prices.

31/10/2024 by ALPHA|1Price targets

Analyst price targets are below the current share price (€14,5).

I think cost reductions, price hedging, increased nuclear output and the divestment of Recycling and Waste will result in €1.60/share for the year (unchanged from 2023).

20/08/2024 by ALPHA|1Geo politics

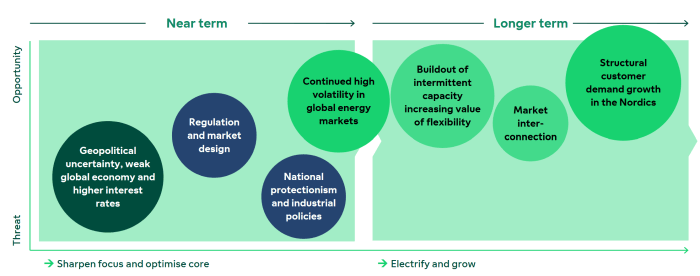

In case of geopolitical escalations (US election, Russia, Middle East) I consider Fortum a relative save and defensive investment. There are many different scenarios that could develop with any escalation. My estimate is that the downside risk for Fortum is relative limited.

20/08/2024 by ALPHA|1

Business (3)

Nuclear power

In 2022 Fortum started a feasibility study for conventional nuclear energy and SMR(s) as future power sources. In a first report it concludes that the market has room for both. Another important conclusion is that risks should be mitigated by utilizing proven solutions/designs. Further more a risk-sharing model is needed as catalyst to spark the investment.

The Finnish Government’s granted a new operating license for both units at Fortum’s Loviisa nuclear power plant until the end of 2050.

With the current price volatility caused by intermittent renewable energy sources it is not possible to calculate a business for investment in new (nuclear) capacity.

The Swedish government published a study that contains possible conditions to facilitate investments in nuclear power; using government funding and price guarantees.

30/10/2024 by ALPHA|1Electricity demanD

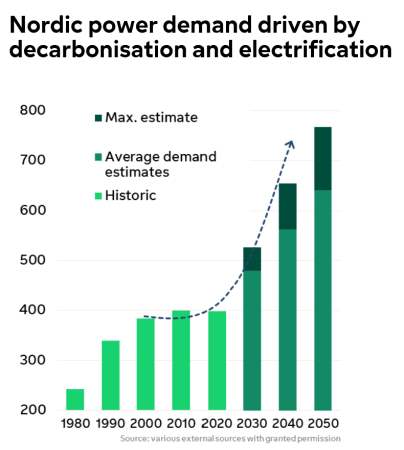

The energy demand is expected to grow driven by electrification; industry (metal, aluminium, hydrogen, etc), data centers (14Twh), and electrical cars. Demand by data centers is expected to increase in the short term. Increased industry demand has a longer time horizon.

The growing industry demand requires stable energy input prices for the investment business case, which increases the demand for fixed prices. The hedging enables Fortum to stabilize its revenue and cash-flow. The results will be less sensitive for the volatility in the electricity prices.

Renewable energy demand is predicted to increased with 5% CAGR in the coming decade.

20/08/2024 by ALPHA|1Clean energy

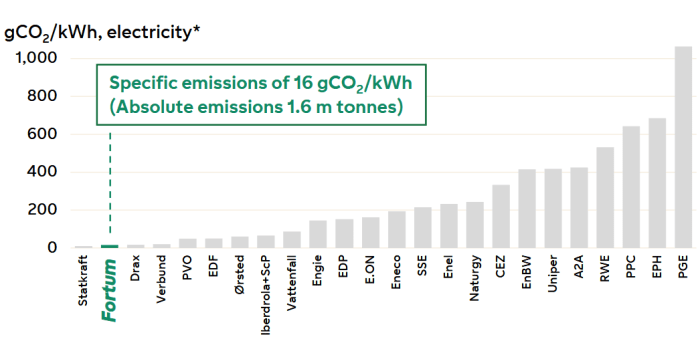

Fortum's produces clean energy from base-load and flexible production sources. This enables the company to realize a €6-8 optimization premium. With the low CO2 footprint the energy produced has a premium value for the industry in the green transition.

20/08/2024 by ALPHA|1

20/08/2024 by ALPHA|1

People (1)

CEO

Markus Rauramo communicates a prudent strategy with sound capital allocation for Fortum. His presentation of the new strategy gives confidence. The CEO repeatedly states that capital allocation for market risk mitigation have priority before cash returns to shareholders.

On the other hand, in 2020 he has been driving the Uniper acquisition together with the previous CEO, which turned into a disaster in 2022. Furthermore he has been leading investments into recycling and waste, that are no longer considered core business.

30/10/2024 by ALPHA|1

Financial (2)

Profitability

Before 2020 the average electricity price was around €35/MWh. After a turbulent time (2021-2023) with volatile price shocks it now looks that prices are coming back to more normal levels. 10-15y historical earnings show that Fortum can also realize good margins at normalized price levels.

Strategy and CAPEX are focused on operational improvement. A program is started to reduce fixed costs with €100M by end of 2025. Operational margins are expected to improve.

Base-load and flexible energy enable an expected optimization premium €6-8/MWh. Fortum is better positioned, through PPA and hedging, for more predictable results in a volatile market.

In the coming years I expect Fortum to improve its ROE (>15%).

02/01/2025 by ALPHA|1Financial strength

The company has a strong balance sheet with a low net debt (0.4x EBITDA). Capital allocation is disciplined and capital expenditure are low (total €1.7B 2024-2026 excl. acquisitions).

Current balance sheet gives room to invest into profitable opportunities (2.0-2.5 EBITDA target). Smaller investments into renewable energy will not immediately increase debt or change capital allocation. There will however be a significant capital demand in case of new nuclear power investments.

30/10/2024 by ALPHA|1

Risks (3)

Regulation

Energy companies are at risk for regulations on maximum price levels.

In 2023 the Polish government set a price cap for end users.

20/08/2024 by ALPHA|1Volatility

High volatility with a risk for lower margin's (on spot prices). The volatility in electricity prices increased due to increased intermittent supply and increased interest for spot contracts by consumers.

20/08/2024 by ALPHA|1Nuclear investments

Investment into nuclear power could be driven by political motivations and have a negative impact on shareholder value.

20/08/2024 by ALPHA|1