Research by MICKE

Author: micke

DB had an improvement program running from 2019 to 2022, there is a follow up program until 2025, and DB continues to deliver good results, with significant improvement possibility (Nordic banks are at C/I=50%). There will be significant earning improvements. Capital return will probably increase by 50% YoY until 2026. "guidance of € 1.00 per share in respect of FY 2025, subject to 50% payout". DB has developed well over the last year, up from €9. The current share price around €15, P/E=4,77, gives good room for further increased share price.

Valuation (1)

Increasing profits and dividends

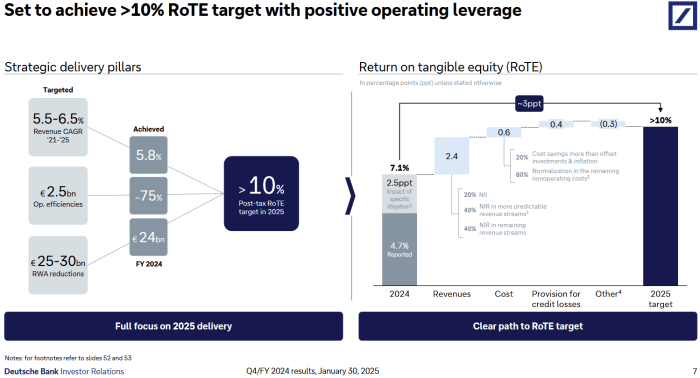

With a 2025 target of RoTE >10% and a P/B=0,42 I see a potential 100% upside from today for the share price, potentially a share price of €30 in 2026/2027.

11/12/2024 by MICKE|1

11/12/2024 by MICKE|1

People (1)

CEO and CFO

The CEO and CFO seem very competent and have greatly improved profitably.

20/04/2024 by MICKE|1

Financial (5)

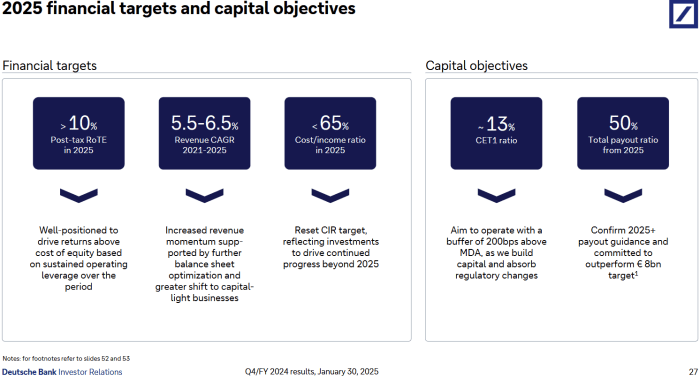

2025 financial targets

Significant improvments from 2024. During 2024 the goal for 2025 was C/I=62,5%, but this was ajusted at 2024Q4 to C/I=65%. The CEO seems very optimistic for 2025.

03/02/2025 by MICKE|1

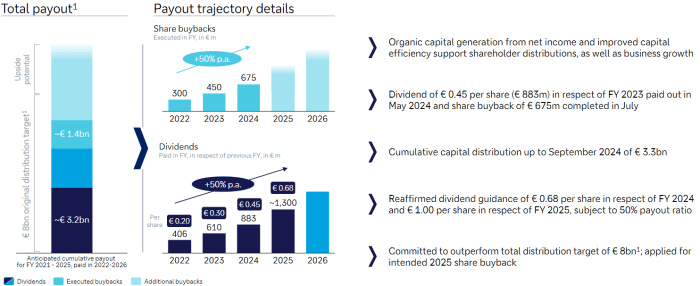

03/02/2025 by MICKE|1Capital distribution, dividends and buy back

DB's target is to distribute €8B for the fiscal years 2021-2025.

Buy-back 2023 H2 450MEUR (50% more than 300MEUR 2022, ~2% or the shares, the dividend was also increased by 50%), based on DB indications during Q1 call, povided DB gets ECB approval.

Poised to accelerate shareholder distributions and to outperform € 8bn target3; dividend

guidance of € 1.00 per share in respect of FY 2025, subject to 50% payout ratio520/04/2024 by MICKE|12023Q3 Outlook by DB:

Expect to achieve FY 2023 net revenues of € 29bn

Q4 2023 earnings likely impacted by a number of positive and negative one-off items

Improved capital outlook creating scope for additional distributions to shareholders

25/10/2023 by MICKE|1Share-related information:Diluted earnings per share €0.61, Tangible book value per basic share outstanding €27.28. DB's goal is to have >10% RoTE (profit post-tax, divided by the tangible equity) in 2025.

17/08/2023 by MICKE|1Earnings and cost efficiencies

DB profit before tax of € 3.3bn after absorbing over € 700m in non operating expenses such as restructuring for operational efficiencies.

"Higher nonoperating costs in H1 2023 with € 0.5bn of litigation expenses to resolve mainly longstanding matters and € 0.3bn restructuring & severance to accelerate strategy"

Earnings per share was €0.63 in Q1 which at share price €10 gives a P/E ~4. DB has a cost efficiency program running and aim at keeping cost fixed while increasing revenue, thus improving C/I ratio. As I see it DB is and will continue to be extremely profitable i.e. cheap at current market cap.

17/08/2023 by MICKE|1

Risks (1)

Only the normal low risks in EU banking

The risks seem to be reasonable, and considering previous problems from 2008 the risk appetite is low.

The market was worried based on US issues, but I don't see that there will be any material effect on DB's business.

03/06/2023 by MICKE|1